Submit a Paper

Submit a Paper Propose a Special lssue

Propose a Special lssue Open Access

Open Access

ARTICLE

A Hybrid CEEMDAN-HOA-Transformer-GRU Model for Crude Oil Futures Price Forecasting

1 School of Civil and Environmental Engineering, Zhengzhou University of Aeronautics, Zhengzhou, 450046, China

2 School of Electronics and Information, Zhengzhou University of Aeronautics, Zhengzhou, 450046, China

* Corresponding Author: Lingxiao Ye. Email:

Energy Engineering 2026, 123(4), 5 https://doi.org/10.32604/ee.2025.072163

Received 20 August 2025; Accepted 16 October 2025; Issue published 27 March 2026

View Full Text

View Full Text Download PDF

Download PDFAbstract

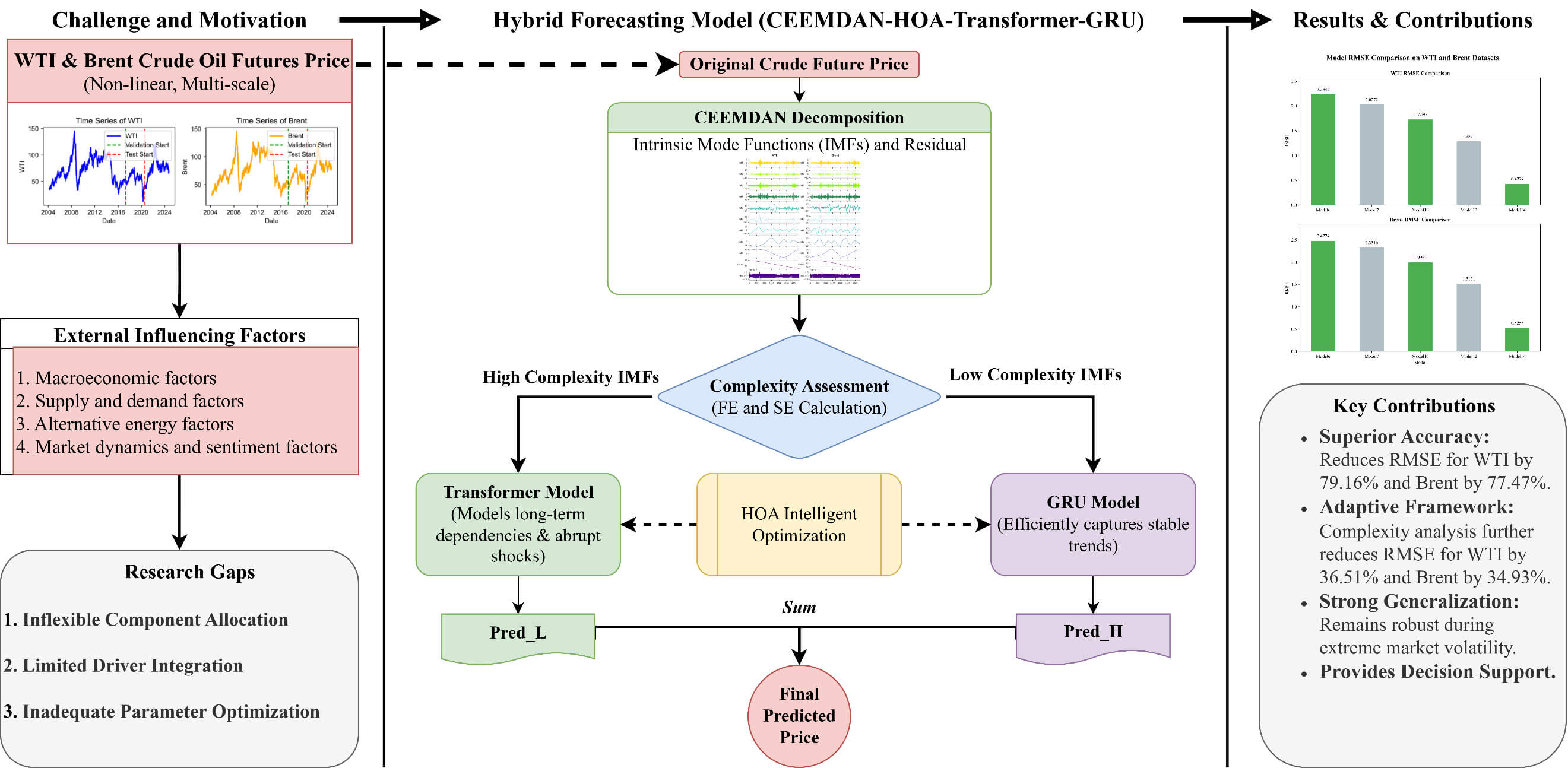

Accurate forecasting of crude oil futures prices is crucial for understanding global energy market dynamics and formulating effective macroeconomic and energy strategies. However, the strong nonlinearity and multi-scale temporal characteristics of crude oil prices pose significant challenges to traditional forecasting methods. To address these issues, this study proposes a hybrid CEEMDAN–HOA–Transformer–GRU model that integrates decomposition, complexity analysis, adaptive modeling, and intelligent optimization. Specifically, Complete Ensemble Empirical Mode Decomposition with Adaptive Noise (CEEMDAN) is employed to decompose the original series into multi-scale components, after which entropy-based complexity analysis quantitatively evaluates each component. A differentiated modeling strategy is then applied: Transformer networks capture long-term dependencies in high-complexity components, while Gated Recurrent Units (GRU) model short-term dynamics in relatively simple components. To further enhance robustness, the Hiking Optimization Algorithm (HOA) is used for joint hyperparameter optimization across both base learners. Empirical analysis of WTI and Brent crude oil futures demonstrates the technical effectiveness of the framework. Compared with benchmark models, the proposed method reduces RMSE by 79.16% for WTI and 77.47% for Brent. Incorporating complexity analysis further decreases RMSE by 36.51% for WTI and 34.93% for Brent, confirming the superior nonlinear modeling capacity and generalization performance of the integrated framework. Overall, this study provides not only a technically reliable tool for modeling complex financial time series but also practical guidance for improving the accuracy and stability of crude oil price forecasting, thereby supporting market monitoring, risk management, and policy formulation.Graphic Abstract

Keywords

Crude oil futures price; CEEMDAN; complexity analysis; transformer; hybrid forecasting model

Cite This Article

APA Style

Guo, Y., Ye, L., Wang, X., Wu, D., Wang, Z. et al. (2026). A Hybrid CEEMDAN-HOA-Transformer-GRU Model for Crude Oil Futures Price Forecasting. Energy Engineering, 123(4), 5. https://doi.org/10.32604/ee.2025.072163

Vancouver Style

Guo Y, Ye L, Wang X, Wu D, Wang Z, Wang H. A Hybrid CEEMDAN-HOA-Transformer-GRU Model for Crude Oil Futures Price Forecasting. Energ Eng. 2026;123(4):5. https://doi.org/10.32604/ee.2025.072163

IEEE Style

Y. Guo, L. Ye, X. Wang, D. Wu, Z. Wang, and H. Wang, “A Hybrid CEEMDAN-HOA-Transformer-GRU Model for Crude Oil Futures Price Forecasting,” Energ. Eng., vol. 123, no. 4, pp. 5, 2026. https://doi.org/10.32604/ee.2025.072163

Copyright © 2026 The Author(s). Published by Tech Science Press.

Copyright © 2026 The Author(s). Published by Tech Science Press.This work is licensed under a Creative Commons Attribution 4.0 International License , which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

Downloads

Downloads

Citation Tools

Citation Tools